PEPE0.00 1.76%

PEPE0.00 1.76%

TON2.98 -0.31%

TON2.98 -0.31%

BNB592.83 0.14%

BNB592.83 0.14%

SOL139.19 -0.26%

SOL139.19 -0.26%

XRP2.06 -1.57%

XRP2.06 -1.57%

DOGE0.16 -2.12%

DOGE0.16 -2.12%

TRX0.24 0.71%

TRX0.24 0.71%

ETH1590.16 -0.73%

ETH1590.16 -0.73%

BTC84506.12 -1.04%

BTC84506.12 -1.04%

SUI2.12 -1.36%

SUI2.12 -1.36%

This report was written by Tiger Research, examining Asia's Web3 regulatory developments in Q1 2025, highlighting progress in Japan, South Korea, Hong Kong, Singapore, Vietnam, and Thailand as these nations establish structured frameworks for cryptocurrency adoption.

TL;DR

-

Major markets push Web3 into formal finance: Japan, Korea, Hong Kong, and Singapore are accelerating Web3 integration through tax reforms, asset reclassification, and licensing frameworks.

-

Stablecoins and CBDCs evolve in parallel: Japan and Hong Kong expand private-sector stablecoin markets, while Korea advances public-sector CBDC pilots.

-

Emerging markets shift from policy to execution: Vietnam and Thailand move into implementation with sandboxes, cross-border pilots, and collaboration with global firms.

Dive deep into Asia's Web3 market with Tiger Research. Be among the 8,000+ pioneers who receive exclusive market insights.

1. Setting the Stage: Asia’s Web3 Moment

In the first quarter of 2025, Asia’s Web3 market continued to advance. While Western markets remained focused on political and regulatory uncertainty, governments across Asia took concrete steps forward. Across the region, authorities introduced new legislation, issued licenses, launched regulatory sandboxes, and expanded cross-border cooperation.

Key developments include Japan’s tax reform and token classification changes. South Korea began cautiously expanding corporate access. Hong Kong accelerated its licensing process. Singapore continued to advance its role in regional coordination.

Asia isn’t chasing the crypto cycle. It’s laying the foundations for the next chapter of digital finance — one that’s institution-friendly, policy-aligned, and increasingly interoperable across borders. This report offers a country-level analysis of major Q1 2025 updates, with insights for businesses and builders navigating Asia’s evolving Web3 landscape.

2. Japan: Quiet Precision, Bold Moves

Japan’s Web3 strategy reflects a pattern of quiet precision—gradual but deliberate progress led by financial institutions. Recently, the government has taken a more active role by opening markets and advancing regulatory frameworks.

In the first quarter of 2025, Japan expanded its role to the international stage. The Asia Web3 Alliance submitted a proposalto the U.S. SEC’s Crypto Task Force, calling for deeper U.S.–Japan cooperation on token classification and cross-border regulatory standards.

While incremental, these steps signal Japan’s intent to participate in shaping global Web3 governance. The objective is not only to clarify domestic policy, but also to contribute to the development of international regulatory norms.

2.1. Crypto Tax Reform: Lower Rates, Deferred Taxation, Legal Clarity

LDP lawmaker Akihisa Shiozaki introduced a plan to reduce the tax rate. Source: @AkihisaShiozaki

In Q1 2025, Japan took steps to improve the regulatory environment for its Web3 sector.The ruling Liberal Democratic Party proposeda revision to the crypto tax regime, including a flat 20% capital gains tax to replace the current progressive rate, which can reach up to 55%.The proposal also introduces a deferral of taxation on crypto-to-crypto transactions—such as exchanging Bitcoin for Ethereum—until the assets are converted to fiat currency.

The initiative aims to reduce tax complexity and establish a clearer framework for both investors and businesses. Although the 20% rate represents a step forward, it remains less competitive than jurisdictions such as South Korea, where capital gains on crypto assets are currently exempt. However, Japan’s focus on legal certainty may attract companies that prioritize regulatory predictability over lower tax burdens.

2.2. Regulatory Classification: Bringing Crypto Into Traditional Finance

On the regulatory side, the Financial Services Agency(FSA) announced plansto reclassify crypto as a financial instrument by 2026. That might sound technical, but it’s a meaningful shift: it brings crypto into the same legal framework as traditional securities, with rules around insider trading and investor protections.

This signals Japan’s intent to position digital assets within the formal financial system, rather than treating them as speculative assets outside regulatory norms. For institutional participants, this shift introduces clearer legal standards and enhanced credibility. However, for smaller teams and DeFi developers, increased oversight may introduce operational constraints. The challenge lies in aligning with evolving regulatory expectations while innovation in the sector continues to outpace policy development.

2.3. Stablecoin Momentum: New Phase in Japan’s Stablecoin Market

Announcement from Circle’s CEO. Source: X(@jerallaire)

Japan also made progress on the stablecoin front. In a key infrastructure move, Circlepartnered with SBI Holdings to bring USDC to Japan — making it the first foreign-issued stablecoin to operate under the country’s 2023 stablecoin law. SBI’s exchange also became the first licensed Electronic Payment Instruments Exchange Service Provider supporting foreign stablecoins.

Further momentum came through a memorandum of understanding signedbetween SMBC, Ava Labs, and several Japanese partners to explore the issuance of both yen- and dollar-denominated stablecoins.

This development reflects growing momentum in the stablecoin sector, where traditional financial institutions are starting to play a bigger role. In parallel, domestic projects like Progmat are gaining traction, suggesting Japan is becoming a competitive — albeit heavily regulated — environment for stablecoin innovation.

3. South Korea: Cautious Signals Toward Regulatory Easing

3.1. New Capital Emerges: Limited Opening for Institutional Investors

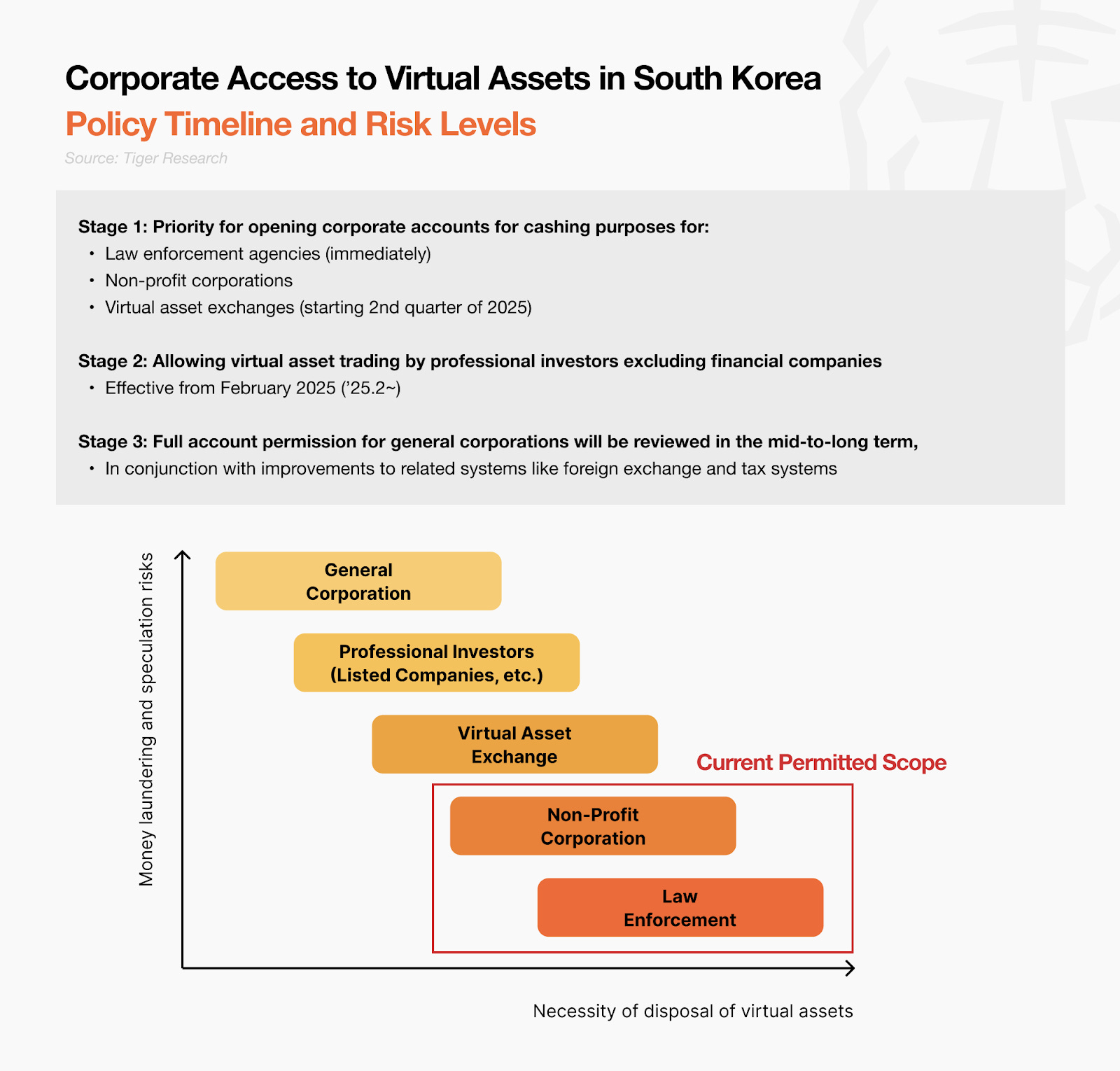

Source: Tiger Research

South Korea made some quiet but important moves on the regulatory front in Q1 2025. One of the most anticipated was a loosening of the corporate crypto trading ban. The Financial Services Commission (FSC)announced that certain approved entities — like law enforcement agencies, universities, and nonprofits — can now sell their crypto holdings to convert them into cash. However, these institutions still face restrictions—they are allowed to sell digital assets but cannot purchase them. This isn’t a full reopening — it’s more like a narrow off-ramp for institutions holding crypto from earlier programs or donations.

A more meaningful shift may come later in the year. A pilot program, set to launch in the second half of the year, will allow a small group of publicly listed companies to trade digital assets under capital markets regulations. But even that will likely come with tight guardrails. For now, this is less about embracing institutional adoption and more about creating a controlled environment.

3.2. CBDC Pilot: Real-World Testing at Scale

Source: Shinhan Bank, Tiger Research

At the same time, the country took a big step forward in its CBDC strategy. In March, the Bank of Korea launched a pilotinvolving 100,000 consumers and seven major banks. The pilot aims to simulate real-world payment scenarios and assess the infrastructure required for potential national deployment. As part of the program, retailers such as 7-Eleven South Korea will accept CBDC payments.

Unlike regional peers such as Japan, Singapore, and Hong Kong—which are primarily focused on developing stablecoin frameworks—South Korea continues to prioritize CBDC development as its primary digital currency initiative.

3.3 Ban on Unlicensed Platforms: A Firm Stance on Investor Protection

While some doors are starting to open, others remain tightly shut. In March, Korean regulators ordered Google to remove 17 unlicensed crypto exchange apps — including Poloniex, KuCoin, and MEXC — from the Play Store. The move reinforced the FSC’s firm stanceagainst unauthorized platforms operating without local registration.

This approach reflects the Korean government’s dual-track policy: gradual openness in areas such as institutional participation and CBDC development, alongside a consistently strict stance on investor protection. For Web3 companies, Korea is no longer an inaccessible market—but it is far from fully open. Opportunities exist, but they favor companies that build infrastructure aligned with local compliance standards.

4. Hong Kong: Full-Speed Regulation, Institutional-Friendly Market

4.1. From Roadmaps to Action: A-S-P-I-Re Sets the Tone

In Q1 2025, Hong Kong acceleratedits push to become a leading crypto hub in Asia through regulatory initiatives and institutional collaborations.

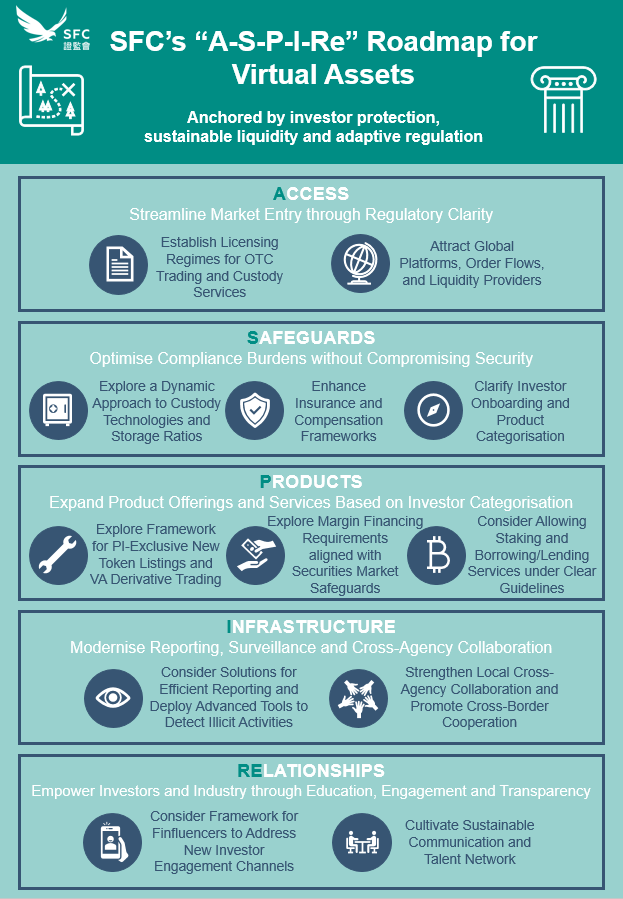

Source: SFC

In February, the Securities and Futures Commission (SFC) unveiled the "A-S-P-I-Re" roadmap, a strategic framework aimed at enhancing Hong Kong’s virtual asset market.This roadmap focuses on five key pillars: Access, Safeguards, Products, Infrastructure, and Relationships. Its 12 initiatives include plans to establish licensing regimes for over-the-counter (OTC) trading desks and custody service providers, as well as consultations on permitting crypto derivatives trading and margin lending within a regulated environment.

This approach follows the principle of “same business, same risks, same rules,” aiming to integrate traditional financial safeguards into the virtual asset sector while accounting for its unique characteristics.It reflects Hong Kong’s long-standing financial legacy and may position the city as one of the first jurisdictions to support experimental financial products within a regulated framework.

4.2. Licensing Momentum: Exchanges Are Going Live

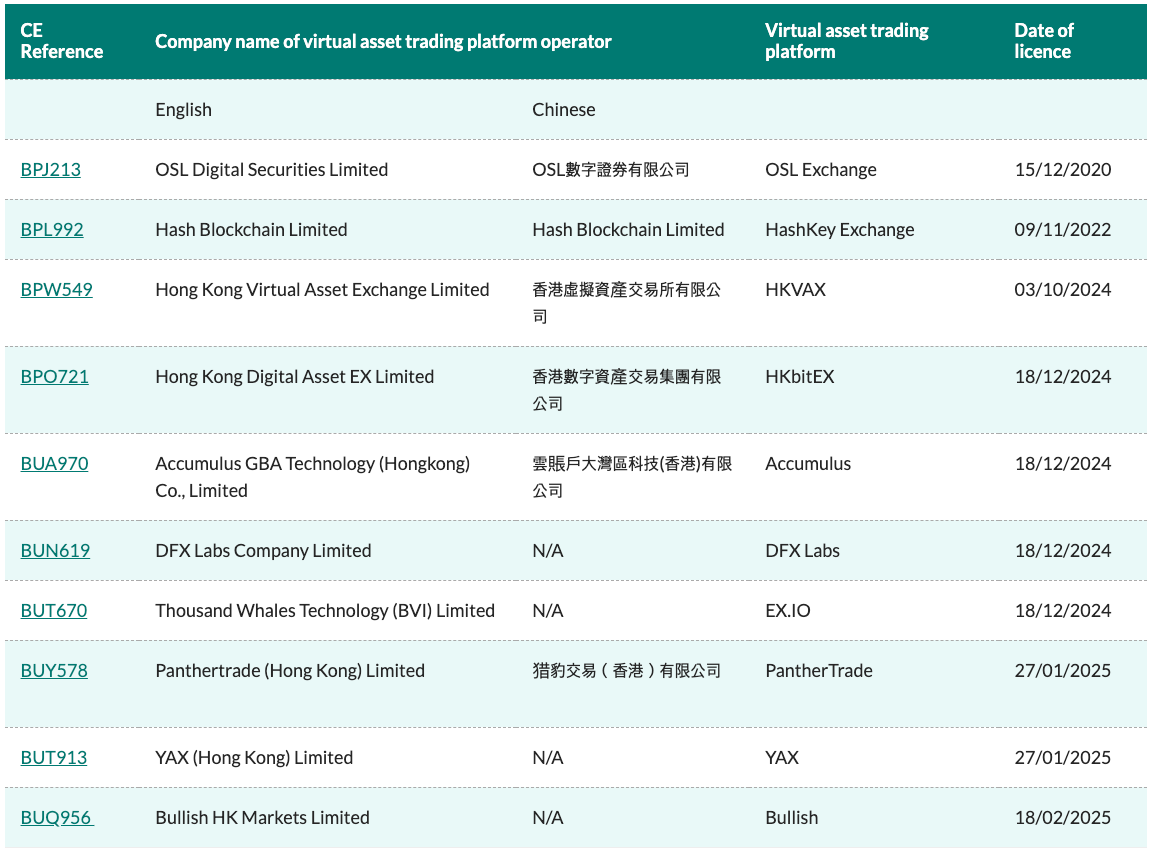

Source: SFC

Building upon the retail exchange licensing framework introduced in 2023, the SFC has approveda total of ten virtual asset trading platform licenses by the end of Q1 2025.For example, Bullish HK Markets Limitedsecured licenses in February 2025, enabling it to operate as a virtual asset trading platform under Hong Kong's regulatory framework.

With these licenses now active, Hong Kong’s framework has moved beyond pilots — it’s live, functioning, and growing. With licenses now active, compliant exchanges can actually launch and operate under a clear, enforceable rulebook. For Web3 business, this opens the door not just to going live, but to building out a broader range of services. With consultations already underway on crypto derivatives, lending, and more, Hong Kong is gearing up to be one of the few places in the world that offer a fully regulated, end-to-end environment for digital assets.

4.3. Stablecoins Next: Big Names Join the Playbook

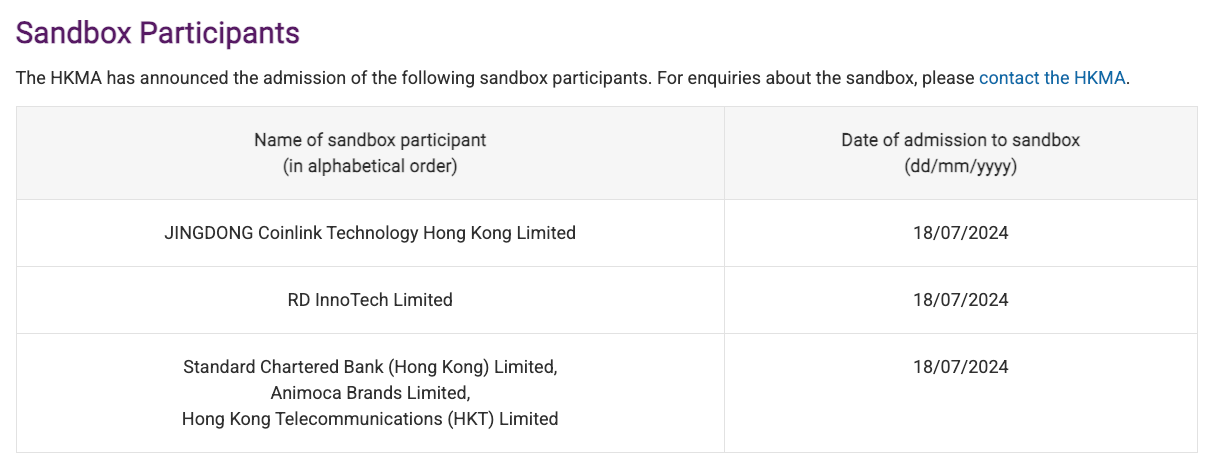

Source: HKMA

Also in February, Standard Chartered Bank Hong Kong, Animoca Brands, and Hong Kong Telecommunications (HKT) announced a joint ventureto issue a Hong Kong dollar-backed stablecoin, pending regulatory approval. The move brings together one of the world’s biggest banks with one of Web3’s most prominent venture players — a rare but powerful signal of institutional alignment around digital assets.

Hong Kong is simultaneously strengthening its private stablecoin infrastructure and conducting CBDC testing through Project Ensemble. This dual-track approach reflects a comprehensive strategy to develop a digital currency ecosystem. By engaging both the public and private sectors, Hong Kong is actively exploring the viability of multiple digital currency models.

5. Singapore: Structure Over Speed

5.1. Institutional Licensing Momentum: Fit Over Fame

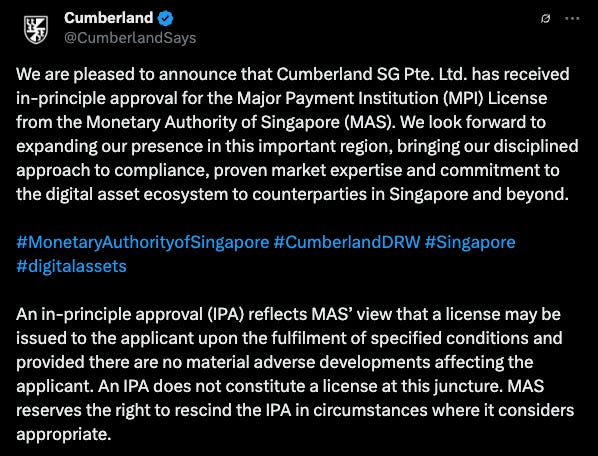

Source: X (@CumberlandSays)

Hex Trustreceived a Major Payment Institution (MPI) license from the Monetary Authority of Singapore (MAS), allowing it to offer cross-border crypto transfer services. Around the same time, Cumberland SG, the Asia division of U.S.-based trading firm Cumberland, secured in-principle approval for its MPI license, adding to the list of institutional players that are deepening their presence in Singapore.

These licensing moves aren’t about volume — they’re about signaling. MAS isn’t courting the names or chasing hype; it’s rewarding firms with clean corporate structures, global reputations, and tight compliance frameworks.While other markets focus on retail momentum or looser innovation zones, Singapore is carving out a role as the region’s policy anchor.

This approach signals that Singapore is not building a sandbox for early-stage innovation but establishing an environment for long-term, institutional-grade operators.

5.2. Regional Diplomacy: Singapore–Vietnam Agreement

In a notable international development, Singapore and Vietnam signed a Letter of Intentto cooperate on digital asset regulation and oversight. The agreement, led by MAS and Vietnam’s State Securities Commission, aims to foster collaboration on regulatory frameworks, supervision, and industry standards — reinforcing Singapore’s role as a regional leader in crypto policy diplomacy.

This isn’t just goodwill diplomacy — it’s Singapore actively exporting its regulatory model. By partnering with fast-moving neighbors like Vietnam, MAS is helping to shape a regional ecosystem where regulatory alignment starts with Singapore.

For Web3 businesses, this kind of diplomacy matters. It means that building with Singapore in mind could offer not just access to one market — but compatibility across many. As other ASEAN markets move from experimentation to formalization, Singapore’s policy leadership is quietly becoming one of its most powerful exports.

5.3. Global Appeal: Robinhood Chooses Singapore

Singapore’s clarity and credibility continue to attract global players. In Q1, U.S. fintech platform Robinhoodannounced plans to roll out crypto services in Singapore by late 2025. Backed by its recent acquisition of Bitstamp, the move highlights Singapore’s appeal to global firms seeking to launch in Asia under a clear and structured regulatory environment.

Robinhood’s entry isn’t just another license win, it reflects a bigger trend. More global fintechs are now choosing Singapore as their regional base, using its clear rules and strong oversight as a foundation for long-term growth. With assets like Bitstamp in hand, they’re doubling down on compliance-first expansion.

In the future, any Web3 company eyeing Southeast Asia may follow the same playbook: start in Singapore for regulatory clarity, then expand into neighboring markets as the regional frameworks mature.

To conclude, Singapore isn’t trying to win the race by moving fast — it’s trying to win by making the rules. In a fragmented regional landscape, its approach is becoming the benchmark: high trust, low risk, and full transparency. That may not attract every startup, but it’s exactly what serious capital, institutions, and cross-border builders are looking for.

6. Vietnam: From Policy Talk to Policy Action

6.1. Legal Framework: Beginning to Take Shape

Vietnam took concrete steps in Q1 2025 toward formalizing a comprehensive legal frameworkfor digital assets. In March, Prime Minister Phạm Minh Chính’s Directive No. 27/NQ-CP mandated the development of crypto-specific regulations by mid-year, with provisions expected to cover asset classification, licensing requirements, AML/KYC compliance, and consumer protection mechanisms.

Concurrently, the government is advancing plans to establish a dedicated financial hub—likely in Ho Chi Minh City—which will include a regulatory sandbox for fintech and cryptocurrency innovation. A pilot program for licensed centralized exchanges is already underway, with a targeted launch in 2026.

Historically, Vietnam has been characterized by robust retail crypto adoption but operated within a regulatory gray area, with prior initiatives failing to translate into enforceable frameworks. The current efforts signal a pivotal shift: Vietnam is transitioning from a passive observer to an active architect of its crypto ecosystem. While full regulatory clarity may take 12–18 months to materialize, the top-down momentum underscores a deliberate and structured approach to fostering a compliant digital asset market.

6.2. Policy Meets Market: Government & Industry Engagement

On March 27, the Vietnam Blockchain Association (VBA) hosted a high-level conference focused on centralized exchange oversight—marking a significant milestone in the country’s regulatory development. The event brought together representatives from key government agencies, over 30 financial institutions, and global exchange operators including Binance, OKX, and Bybit.

Discussions covered core regulatory issues such as taxation, cybersecurity, stablecoin governance, and FATF compliance. The breadth and depth of topics highlighted an emerging alignment between policymakers and industry stakeholders.

Mr. Nguyễn Thế Vinh presented at a seminar on the digital economy and digital transformation. Source: Znews

The government’s engagement reflects a shift from passive rulemaking to active collaboration in shaping market infrastructure. This approach underscores Vietnam’s intent to formalize the role of digital assets within its financial system, with transparency and regulatory clarity as central goals. Although launching a domestic exchange remains complex amid global competition, the ongoing dialogue lays the groundwork for a more structured and competitive digital asset market.

6.3. Traditional Finance Dips In: VBA–Dragon Capital Partnership

Strategic partnership signing between Vietnam Blockchain Association and Dragon Capital. Source: Nguoiquansat.vn

The conference also marked a notable partnershipbetween the VBA and Dragon Capital, a leading asset manager with approximately $6 billion in assets under management. The collaboration focuses on research related to tokenized ETFs. With Thailand advancing regulatory approval for crypto ETFs, the emergence of a regulated product in Vietnam appears increasingly plausible.

Despite this progress, Vietnam’s regulatory environment remains incomplete. A comprehensive framework for licensed and compliant operations is still pending, and is unlikely to be finalized until the upcoming crypto law and regulatory sandbox are implemented. As a result, Vietnam may not yet be suited for launching fully regulated operations.

However, the market remains attractive for development. Vietnam offers a strong retail user base, an expanding pool of developer talent, and growing political momentum. These factors present a favorable environment for Web3 teams to focus on community engagement, build credibility, and position themselves strategically for long-term participation in the market.

7. Thailand: Selective Opening, Clear Boundaries

7.1. Tether and SEC: Stablecoins Approved for Trading

In the first quarter of 2025, Thailand’s Securities and Exchange Commission (SEC) approvedTether’s USDT and Circle’s USDC for trading on licensed digital asset exchanges, effective March 16. The decision followed a public consultation in February, during which most respondents supported the proposal.

The approval of USDT and USDC—two of the world’s largest stablecoins—represents a significant step in Thailand’s broader strategy to advance its digital asset ecosystem. The process also reflected a notable level of regulatory cooperation. Tether engaged directly with Thai authorities to meet compliance requirements and committed to improving its services for local users.

With formal approval in place, exchanges can now offer USDT and USDC as part of their services, facilitating faster settlement, more efficient cross-border transactions, and improved fiat on-ramps for digital assets. This decision also marks one of the few instances where a global stablecoin issuer has worked closely with a national regulator in Southeast Asia.

The move may serve as a reference point for other stablecoin issuers seeking regional expansion and contributes to establishing a regulatory foundation for future digital asset products in Thailand.

7.2. Crypto Sandboxes: Not Green Lights

In February 2025, the Thai government unveiled plans to establish a cryptocurrency sandbox in Phuket, with the initiative set to launch by October 2025. This sandbox aims to provide a controlled environment for testing digital asset payment systems while also shaping future policy frameworks.

The sandbox does not indicate a shift toward full liberalization. Rather, it offers a structured setting for limited experimentation. Initial areas of focus are likely to include tourism-related payments, asset tokenization, and local transaction use cases.

With USDT and USDC now approved for trading, the sandbox presents a timely opportunity to engage global stablecoin issuers such as Tether and Circle. Their participation could introduce institutional-grade infrastructure and demonstrate practical use cases for stablecoin payments within a compliant framework.

Collaboration between regulators and global issuers may accelerate the development of real-world applications, including stablecoin-based tourism payments and merchant settlement systems. In this context, the sandbox functions not only as a policy tool but also as a strategic platform for innovation within Thailand’s evolving Web3 ecosystem.

8. Asia’s Web3 Landscape: Coordinated, Not Chaotic

Asia’s Web3 landscape is not defined by disorder, but by deliberate progression. While each country advances at its own pace, the overall trajectory is consistent—toward greater regulatory clarity, institutional integration, and long-term policy alignment.

For companies operating in the region, the implications are clear. The era of unregulated experimentation is giving way to a more structured environment. Success will depend on the ability to meet compliance requirements, deliver tangible use cases, and adapt to local market conditions.

Future growth in Asia’s Web3 sector will not be driven by exploiting regulatory gaps. Instead, it will come from teams capable of operating within formalized frameworks, forming institutional partnerships, and scaling responsibly. The pathway is becoming more defined—and for those equipped to navigate it, the opportunities are expanding.

Disclaimer

This report has been prepared based on materials believed to be reliable. However, we do not expressly or impliedly warrant the accuracy, completeness, and suitability of the information. We disclaim any liability for any losses arising from the use of this report or its contents. The conclusions and recommendations in this report are based on information available at the time of preparation and are subject to change without notice. All projects, estimates, forecasts, objectives, opinions, and views expressed in this report are subject to change without notice and may differ from or be contrary to the opinions of others or other organizations.

This document is for informational purposes only and should not be considered legal, business, investment, or tax advice. Any references to securities or digital assets are for illustrative purposes only and do not constitute an investment recommendation or an offer to provide investment advisory services. This material is not directed at investors or potential investors.

Terms of Usage

Tiger Research allows the fair use of its reports. ‘Fair use’ is a principle that broadly permits the use of specific content for public interest purposes, as long as it doesn't harm the commercial value of the material. If the use aligns with the purpose of fair use, the reports can be utilized without prior permission. However, when citing Tiger Research's reports, it is mandatory to 1) clearly state 'Tiger Research' as the source, 2) include the Tiger Research logo. If the material is to be restructured and published, separate negotiations are required. Unauthorized use of the reports may result in legal action.